You need money fast. You open an app, see “2.5% interest,” and think that sounds fair. You click accept. Then repayment day comes and the number looks nothing like what you expected. This happens to people every day. Here is why.

The First Thing Loan Apps Do Not Explain

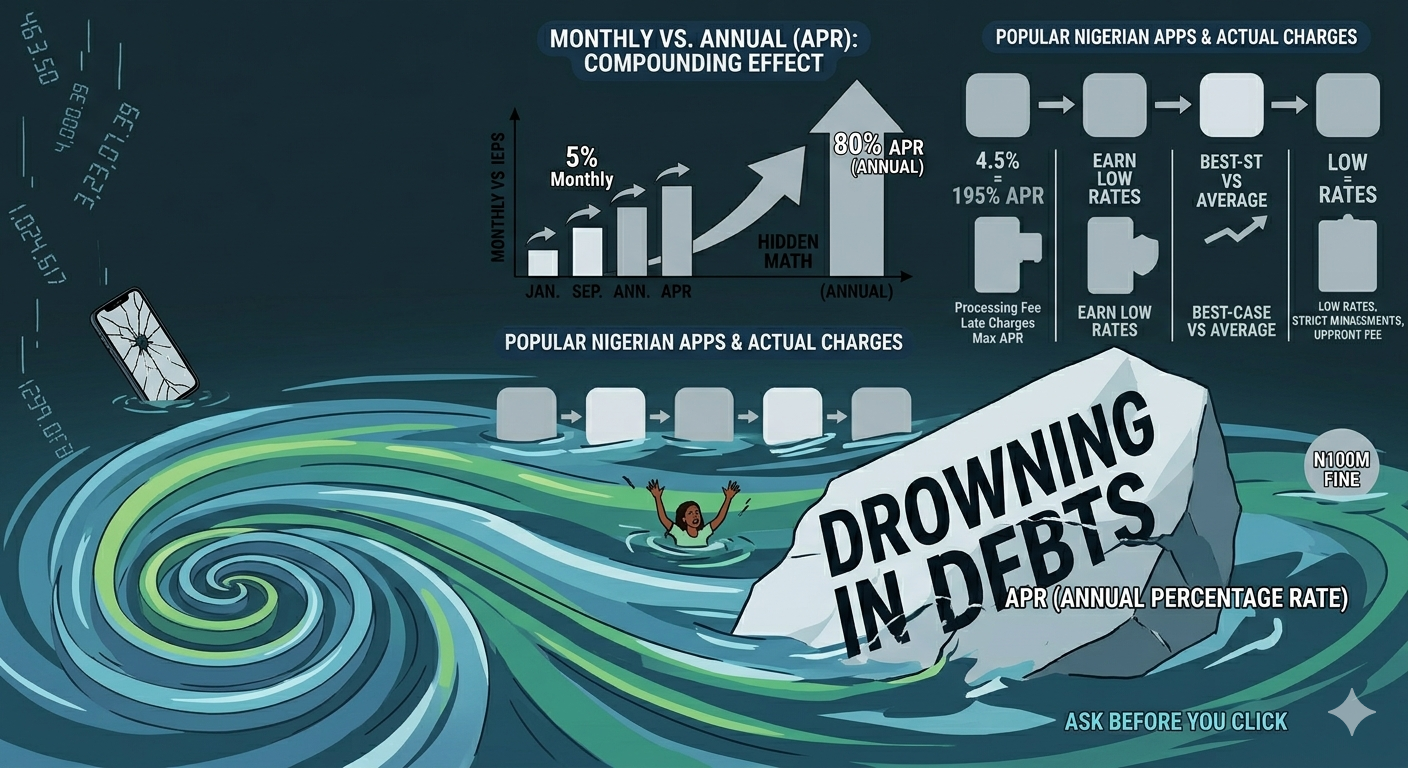

Every loan app shows you a monthly interest rate. The number is always small. 5%. Maybe 10%. What they rarely tell you is what that number actually becomes over a full year.

Here is a simple example. If an app charges 5% every month, that does not mean you are paying 5% per year. By the time compounding is factored in, that 5% monthly rate works out to roughly 80% annually. That is a very different number.

Nobody borrowing in an emergency is sitting down to do that maths. And most apps are not doing it for you either.

What Each Popular App Actually Charges

FairMoney Monthly rate: 2.5% to 30% | Loan range: N1,500 to N1,000,000

FairMoney is one of the biggest loan apps in Nigeria with over 10 million downloads. The 2.5% rate exists, but only for people who have borrowed before and paid back on time. If you are a new user, expect to be on the higher end. To put it plainly: borrow N100,000 for three months at 10% per month and you will repay N130,000 total, which is N43,333 every single month.

Carbon Monthly rate: 4.5% to 30% | Max APR: 195% per year | Loan range: N2,500 to N1,000,000

Carbon is one of the few apps that openly publishes its highest possible APR, which is 195%. That figure sounds big because it is, but at least they say it. In real terms, a N1,000,000 loan over 12 months at the lowest monthly rate of 4.5% means you will repay N1,540,000 by the end. Pay back early and they reward you with a better rate next time.

Palmcredit APR range: 24% to 56% | Loan range: N10,000 to N300,000

On paper, Palmcredit looks like one of the cheaper options. In practice, an 8% monthly rate on a N200,000 loan over six months adds up faster than the headline figure suggests. The low APR they advertise is the best possible scenario, not the average one.

Branch Monthly rate: 2.1% to 12% | Loan range: N2,000 to N500,000

Branch is generally one of the cheapest apps on the market. Instead of asking for documents, it looks at your smartphone data to decide if you qualify. The downside is that new users almost always get the higher rate. The low rates are earned, not given.

Renmoney Monthly rate: 2.12% to 2.65% | APR: 25.44% to 31.8% | Loan range: up to N6,000,000

Renmoney is more like a proper lender than a quick-cash app. Its rates are among the lowest, its loan sizes are the largest, and it is upfront about what it charges. There is also a 1% management fee on top. The trade-off is that not everyone will qualify since it has stricter requirements.

Okash Monthly rate: 3% to 15%

Okash is run by Blue Ridge Microfinance Bank and is mostly used for small, short-term borrowing. The rate you get depends almost entirely on how long you have been using the app and whether you have repaid before. First-time users almost always start at 15%.

The Charges They Mention Last

Interest is not the only thing you pay. Most apps add a processing or management fee before they send you the money. This fee can be anywhere from 1% to 20% of whatever you borrowed, taken upfront.

Then there are late payment charges. If you miss your due date, Carbon for example adds a fee of 0.03333% every single day until you pay. That does not sound like much until you stretch it across a week or two on a large loan.

The One Number You Should Always Ask For

The APR, which stands for Annual Percentage Rate, is the most honest number in lending. It combines interest and fees into one figure that tells you exactly what the loan costs over a full year.

At the cheaper end of the market, apps like Branch and Renmoney sit between 25% and 35% APR for borrowers with good history. At the expensive end, some apps go as high as 264% APR. That is not a mistake. A small short-term loan at a high monthly rate, when stretched into annual terms, can cost more than twice what you borrowed.

If an app refuses to show you the APR before you sign, take that seriously.

What the Government Changed This Year

The FCCPC and the CBN have been pushing digital lenders to behave better. Over 430 lending apps have now been checked for compliance. The rules say apps must show fees clearly, cannot access your full contact list, and cannot call or message your friends and family about your debt. That last one was a real problem for years. It is now illegal, with fines reaching N100 million for apps that still do it.

The market is cleaner than it was two years ago. But nobody has capped the interest rates. A licensed app can still charge you 30% monthly and do so completely legally.

How to Get a Better Deal

The people who get the lowest rates are not the ones in the most need. They are the ones who borrowed before, paid on time, and stayed with the same app long enough to earn a better offer. Carbon, Branch, and FairMoney all have systems that lower your rate and raise your limit the more you prove yourself.

For anything above N5 million, loan apps are not the right option. Look at Renmoney or CreditVille instead. For small first loans under N10,000, Branch and FairMoney can approve you with just your NIN and no BVN.

And before you accept anything, ask what the APR is. Not the monthly rate. The APR. If they cannot give you that number, keep looking.

and then

and then